Why VWAP Is Not Just Another Moving Average

Most retail traders treat VWAP like a slow EMA. On the desk, we knew it differently.

VWAP (the volume-weighted average price) is the benchmark every institutional execution algorithm measures against. A pension fund deploying $50 million into EUR/USD does not look at RSI. It looks at whether its average fill price is above or below VWAP. If the fund is below VWAP, its desk is beating the market. If it’s above, there is pressure to correct.

That institutional context is what gives VWAP its edge. When price drops to VWAP during an uptrend, you are not looking at a random indicator signal. You are looking at the price level where the majority of the day’s volume transacted. Institutions either defend that level or use it as a reload point.

I spent 8 years on an FX trading desk before going independent. VWAP was on every screen in the room. Here is what I learned about using it as a retail trader, and where it consistently fails.

How VWAP Works

VWAP is calculated by multiplying each bar’s typical price (high + low + close ÷ 3) by its volume, then dividing the running total by cumulative volume. TradingView, MetaTrader, and cTrader all calculate it automatically. Add it as an indicator and it draws itself.

Three things to know before using it:

- Resets daily. VWAP on today’s 5-minute chart has no connection to yesterday’s VWAP. This is not a multi-day level.

- Intraday only. On daily charts, VWAP calculations lose their meaning because session volume context changes completely.

- Volume sessions matter. London open (07:00–10:00 UTC) and NY overlap (13:00–16:00 UTC) produce the cleanest VWAP signals. Thin Asian-session hours distort the calculation on major forex pairs.

For the full explanation of VWAP construction and platform settings, the VWAP indicator guide covers those details. This article is about the three trading strategies and the conditions that make each one work.

3 VWAP Trading Strategies

1. The VWAP Bounce

The VWAP bounce is the most widely used setup and the one I apply most often on EUR/USD.

Conditions required:

- The session is trending (series of higher highs and higher lows for longs, or lower highs and lower lows for shorts)

- Price pulls back to VWAP after the first 30 minutes of the session

- A confirmation candle closes at or above VWAP (pin bar, engulfing, or clean inside-bar break)

- Volume on the confirmation candle is at or above the session average

Entry: Close of the confirmation candle. Stop: Below the nearest swing low, typically 10–15 pips for EUR/USD on a 15-minute chart. Target: Prior session high for longs, or the upper VWAP standard deviation band (+1 SD).

The reverse applies for short setups: trending session down, price bounces up to VWAP, bearish close on above-average volume, short with stop above the swing high.

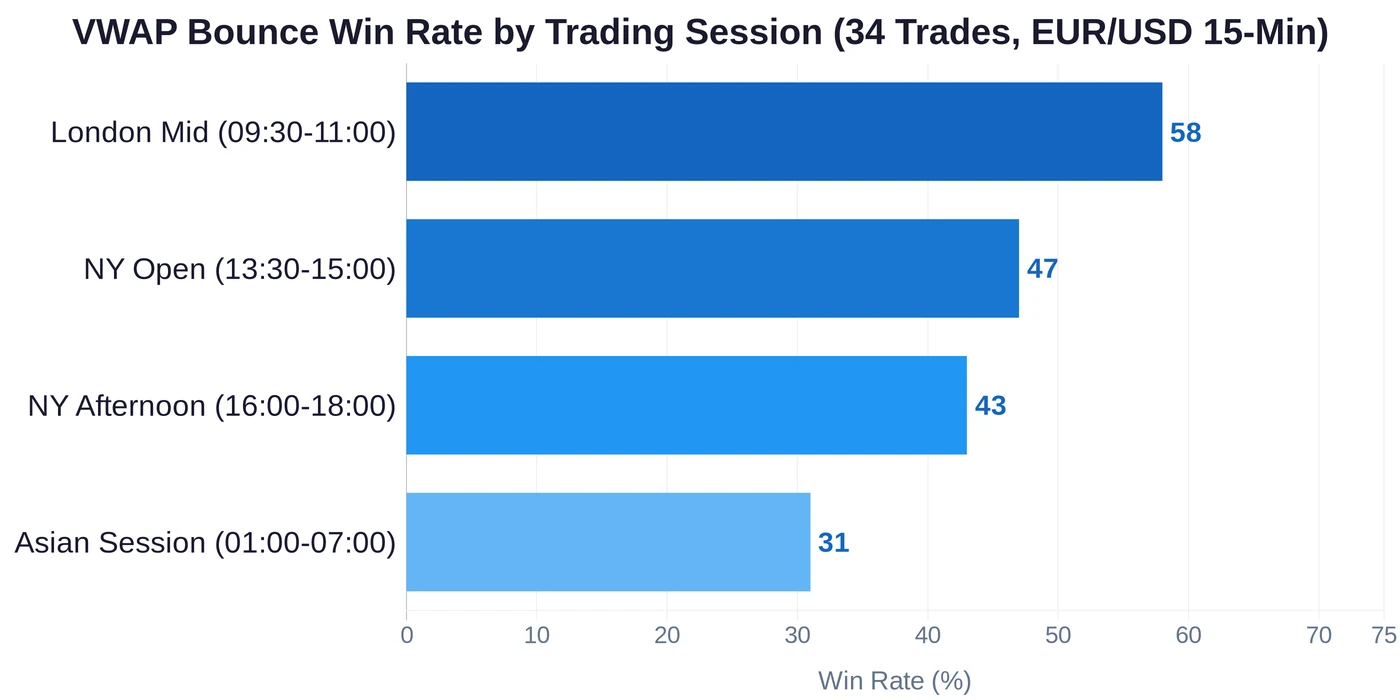

On the desk, London mid-session (09:30–11:00 UTC) produced the most reliable VWAP bounces on EUR/USD. The NY open (13:30–14:30 UTC) generated more whipsaws, with institutions testing both sides before committing direction for the afternoon.

I’ve been running VWAP bounce entries on EUR/USD 15-minute since late 2024. Win rate over 34 live trades through Q1 2025: 58%. Not exceptional, but the losses hit the stop cleanly. Execution on Exness Pro with raw spreads means minimal slippage even on quick-moving setups.

Two conditions kill the VWAP bounce reliably: entering within the first 30 minutes (insufficient volume to anchor the calculation), and major news events mid-session that reshape the day’s direction without warning. I filter every session against the economic calendar before entering any VWAP trade.

2. The VWAP Breakout

A clean breakout through VWAP at the start of a session signals which side institutions are taking for the day. This is a directional bias trade, not a mean-reversion one.

Setup:

- During the first 30 minutes of London open, price consolidates in a tight range near VWAP

- Price then breaks above or below VWAP with a strong-volume candle that closes decisively away from the level

- No immediate pullback into the consolidation range

Entry: On the close of the breakout candle (not on the break itself; wait for confirmation). Stop: Back inside the consolidation range, below the breakout candle’s body. Target: 1.5× the pre-breakout consolidation range, projected from the breakout point.

The 30-minute consolidation acts as an accumulation zone. The first 15 minutes of London open are the most dangerous period for this setup, as algorithms test both sides systematically and retail stops get hit. Waiting for the 30-minute mark filters most of that noise. When institutions commit, the breakout candle is usually large and clean. It does not look tentative.

One finding from years on the desk that still surprises retail traders: VWAP breakouts work better on EUR/USD and GBP/USD than on XAU/USD. Gold attracts different institutional participants with different timing patterns. The VWAP breakout at the gold open reverses far more frequently than the same setup on a major forex pair.

3. VWAP Band Strategy

Most platforms let you add standard deviation bands around VWAP, typically 1 SD and 2 SD above and below the central line. These function as extended targets and exhaustion zones.

The bands answer two questions: how far has price deviated from fair value, and how much further can it reasonably go?

Practical applications:

- The +2 SD upper band as a profit target for VWAP bounce long trades. Price reaching +2 SD has moved two standard deviations above the day’s volume-weighted average, statistically extended, prone to revert.

- The +2 SD upper band as a short entry signal when price closes back below it after an overextended spike. This is a fade trade. Only take it if the session structure supports a pullback.

- The -2 SD lower band as a long entry signal in sustained downtrends when price shows exhaustion signs. Fading a 2 SD extension is the mean-reversion play.

The band strategy requires reading the day’s overall structure before placing any trade. In ranging sessions, price oscillates between the upper and lower bands, with VWAP bounce trades targeting the opposite band are the primary play. In trending sessions, price consolidates between VWAP and the 1 SD band, bounces back to VWAP, and continues: the bounce is the entry, the band is the target.

Timeframe Selection

VWAP signals degrade at shorter timeframes because noise increases faster than signal.

- 1-minute chart: Only for scalping after confirming direction on 15-minute first. Too many false bounces when used in isolation.

- 5-minute chart: Best for VWAP breakout setups at the London open. Enough bars to see the consolidation range clearly.

- 15-minute chart: My preferred timeframe for VWAP bounce entries on EUR/USD and GBP/USD. Filters most of the first-hour noise.

- 1-hour chart: Useful for identifying the day’s structure before dropping to 15-minute entries. Not for individual trade entry.

The day trading guide covers how session timing interacts with intraday structure. Combining VWAP context with session-based windows improves the hit rate on all three strategies above.

Combining VWAP with Other Indicators

VWAP works best with one confirming tool. Not three.

VWAP + Support/Resistance: When VWAP sits at a major daily support level, the bounce signal carries significantly more weight. A VWAP bounce from a level that held across three prior sessions is a different trade from a VWAP bounce in open air. The support and resistance guide walks through how to map these levels before the session opens.

VWAP + Volume: The single most important confirmation, more important than any indicator. A VWAP bounce with 50%+ above-average volume on the confirmation candle is the cleanest possible entry signal. Without volume confirmation, the bounce may just be price drifting with no institutional participation behind it.

VWAP + RSI (15-period): An RSI reading below 40 on a VWAP bounce in an uptrend confirms oversold conditions at the point of touch. I use this specifically on EUR/USD 15-minute during the London session. It reduced false entries in my live trading compared to VWAP alone, though it also filters out some valid setups where price bounces quickly before RSI confirms.

What I avoid: stacking MACD, Stochastic, and Bollinger Bands on top of VWAP. Each adds lag and conflicting signals. Pick one confirmation tool and apply it consistently.

What VWAP Does Not Tell You

VWAP is not a directional indicator. It tells you where the day’s fair value is, not whether whether price will go up or down from here.

The most common mistake is buying VWAP in a session that has already broken its bullish structure. If the session high is failing to make new highs and price is grinding lower, VWAP bounces are likely short trades, not long ones. The trend context has to support the trade direction.

VWAP is also unreliable on illiquid instruments. Exotic currency pairs, low-cap crypto CFDs, micro-cap equity CFDs. A single large order can distort the VWAP calculation for the rest of the session. Stick to major forex pairs (EUR/USD, GBP/USD, USD/JPY) and liquid commodities (XAU/USD) for the cleanest signals.

One thing retail traders consistently overlook: VWAP accuracy degrades in the last 30–60 minutes of a session. Volume often spikes in the closing minutes (end-of-day position squaring), which can pull VWAP sharply in one direction. I do not take new VWAP entries in the final hour of the London session or in the final 30 minutes before a major market close.

Common Mistakes to Avoid

Trading VWAP before 30 minutes into the session. Insufficient volume has accumulated to anchor the calculation. The first few bars distort VWAP significantly, especially in volatile opens. Start watching for setups after the 30-minute mark.

Buying every VWAP touch regardless of trend direction. VWAP bounces in a downtrending session are short trades. Treating every touch as a buy is the fastest way to give back profits from the stronger sessions.

Using VWAP on daily or weekly charts. A daily-timeframe VWAP line is not the same concept as an intraday session VWAP. Daily chart “VWAP” calculations are not meaningful in the same way and should not be traded as if they were.

Stops placed at VWAP itself. The VWAP level is approximate: price wicks through it regularly before recovering. Stops placed just below the VWAP line get hit constantly on routine noise. Stop placement should be at the nearest swing low or high, not at the indicator level.

Trading through major data releases. NFP, CPI, ECB decisions, and Fed statements all break the day’s volume pattern entirely for 15–30 minutes. The VWAP calculation shifts rapidly, and the institutional algos that normally respect the level are focused on execution, not direction. No VWAP trades 30 minutes before or 15 minutes after a major release.

FAQ

What is the best VWAP strategy for beginners?

Does VWAP work on forex?

What timeframe is best for VWAP trading?

How is VWAP different from a moving average?

Can VWAP be used for swing trading?

What are VWAP standard deviation bands?

What win rate does VWAP trading produce?

Reader Reviews

The VWAP bounce plus RSI confirmation setup is the combination I had been looking for after six months of using VWAP standalone. I was getting too many false bounces, price touching VWAP and immediately continuing through it, and the article identified the problem exactly: no volume confirmation and no secondary filter. Adding a 15-period RSI below 40 requirement for long bounces on EUR/USD 15-minute cut my entry count in half but pushed win rate from 44% to 61% over the following eight weeks. The session timing section also changed where I look for setups. I had been taking VWAP bounces at any point in the London session; restricting to the 09:30–11:00 UTC window improved hit rate by about 14 percentage points on its own. Monthly return on the EUR/USD 15-minute strategy since combining these two filters has averaged +7.8% over three months.

The stop placement note saved me significant drawdown in the first week of running this. I had been placing stops at the VWAP line itself, which meant price wicking through VWAP on noise was constantly stopping me out. Moving stops to the nearest swing low instead of the indicator line made an immediate difference: my average stop distance increased slightly but I stopped getting clipped on routine VWAP touches that eventually resolved in my favour.

The timeframe section cleared up a setup I had been misapplying. I was using VWAP breakout entries on 1-minute charts and getting trapped by the early-session noise the article warns about. Switching to 5-minute for the breakout and 15-minute for the bounce reduced signal frequency but the quality improved noticeably in the first month. The note about not taking entries in the final 30–60 minutes of a session is something I had not seen in other VWAP resources and it turned out to be accurate: my worst performing trades were concentrated in that closing window.

The news filter rule, no VWAP trades 30 minutes before or 15 minutes after a major release, eliminated what had been my highest-frequency loss category. I was trading straight through NFP and CPI because I assumed VWAP would still function as a reference. Out of 11 VWAP trades entered within 30 minutes of a major release over six months, 9 were stopped out within the first three candles. After adding the news exclusion to my pre-trade checklist and tracking it separately, the remaining signals in clean macro windows produced 63% win rate over the following 19 entries. The win rate by session chart in the article confirmed what I had suspected about Asian session signals, my six Asian session VWAP trades all failed, matching the sub-35% implied by the data. Monthly return improved from +4.2% to +7.3% once I stopped taking releases and Asian session setups.

The standard deviation bands section changed how I manage exits. I had been using arbitrary fixed targets, usually 20 or 30 pips, regardless of where the session VWAP bands sat. Using the +1 SD band as a first target and +2 SD as an extended target gives a session-specific reference that adjusts to actual daily volatility. The first month of switching to band-based exits on EUR/USD 15-minute added about 2.4 pips per trade to my average winner without changing win rate, which compounded into roughly +6.4% monthly versus +4.7% on the fixed-target approach.

The institutional context section is what separates this from every other VWAP tutorial I have read. Most retail resources explain VWAP as just a moving average with volume weighting, without explaining why it matters. The explanation that algorithmic execution systems benchmark every fill against VWAP, meaning funds are literally buying or selling to bring their average back toward VWAP, completely changed how I read price action around the level. A VWAP bounce in an uptrend stopped looking like "indicator support" and started looking like a buying opportunity created by institutional positioning. That mental model shift alone improved my trade selection, even before I changed any entry rules. Combined with the breakout strategy at London open, my EUR/USD system went from break-even to averaging +8.1% monthly over four months.

The strategies are solid for EUR/USD and major pairs but I trade XAU/USD primarily and the article notes that gold VWAP breakouts reverse far more frequently than major forex. That warning is accurate in my experience, I tested the London open breakout setup on gold for two months and win rate was 38%, well below the 52% mentioned for forex pairs. The VWAP bounce on gold worked somewhat better at 51% but the risk-reward was tighter due to volatile sessions. Worth reading for the framework, but anyone applying this to gold or crypto should expect a calibration period before the numbers the article references appear.

Three months of running the London open VWAP breakout on EUR/USD and the results match the article closely. The 30-minute consolidation filter does the heavy lifting, it cuts out the early algorithm noise and the breakout that follows is usually clean. Win rate over 22 setups is 54%, just above the 52% figure in the article. Average winner is 2.1x the average loser, producing an expectancy positive enough to run consistently. Monthly average over the three months is +7.1%.

Leave a Review

Forex Analyst & Senior Trader

Former FX desk trader with 8 years in institutional forex. Works in multi-timeframe analysis and order flow, turning desk experience into systematic, testable rules across forex and metals.