Is Forex Trading Profitable in 2026? Real Numbers and What Separates the 20%

Why most retail traders lose

In December 2024 I tracked a publicly shared MyFXBook account that had compounded a $1,500 deposit to $4,200 over five months. The trader was running 1:2 risk-to-reward on EUR/USD, 0.05-0.08 lots per trade, 71% win rate across 213 trades. By any measure a profitable trader. Then in week one of January, three losing trades hit in three days, and rather than accept a normal drawdown the account was suddenly running 0.3 lots on a single EUR/USD position with the stop moved twice. Two days later the account closed at $480. Five months of patient compounding eliminated in 96 hours of revenge trading.

That story is the model, not the exception. Most retail losses aren’t slow erosion. They are concentrated in a handful of bad decisions after a string of normal losing trades. The trader who was profitable for five months wasn’t lacking strategy — he was lacking the rule that would have prevented him from sizing up after a drawdown. Risk management is the difference between a profitable retail trader and a blown account, and it’s the single variable that the 20-30% who survive long-term get right.

The numbers are uncomfortable. The European Securities and Markets Authority requires regulated brokers to disclose how many retail clients lose money. Across major regulated brokers in the EU and UK, that figure runs between 70% and 80%.

That’s not a reason to avoid forex. It’s a reason to understand what separates the 20-30% who profit.

After 8 years on an FX trading desk and 4 years managing my own account independently, I’ve watched both sides up close. The losses almost always come from the same places:

- Oversized positions relative to account balance

- Trading strategies with no real backtested edge

- Letting losers run while cutting winners short

- Expecting too much, too fast, from too small an account

None of this is a secret. The problem is that most traders learn these lessons by losing money rather than reading about them.

What profitable forex trading actually looks like

Let me give you a concrete example rather than theory.

The setup I trade is EUR/USD trend-following on the daily chart, combined with COT (Commitment of Traders) data to see where institutional money is positioned. Boring setup. Proven numbers. Over 4 years of backtesting: 68% win rate, average risk-to-reward of 1.5, roughly 8-12 trade setups per month.

On a $600 account trading 0.02 lots with 1% risk per trade, that works out to 6-8% monthly during trending conditions. In choppy months, 4-6 setups may produce flat results. That’s expected: the edge only becomes statistically meaningful after 50+ trades.

I run this on Exness Pro, where raw spreads on EUR/USD start from 0.0 pips plus $3.50 commission per lot. Transaction costs matter more than most beginners realise. On a standard spread account, you give back 0.7-1.3 pips to the broker on every entry, which adds up across hundreds of trades per year.

The finding that surprised me most: trend-following performs better on the daily timeframe than intraday. On the desk, we watched retail traders grind 15-minute charts hunting quick wins. The noise on short timeframes degrades edge fast. The daily chart filters most of it out.

A realistic profit expectation

The most common mistake beginners make is expecting 30-50% monthly returns. That’s not forex — that’s a signal seller’s pitch.

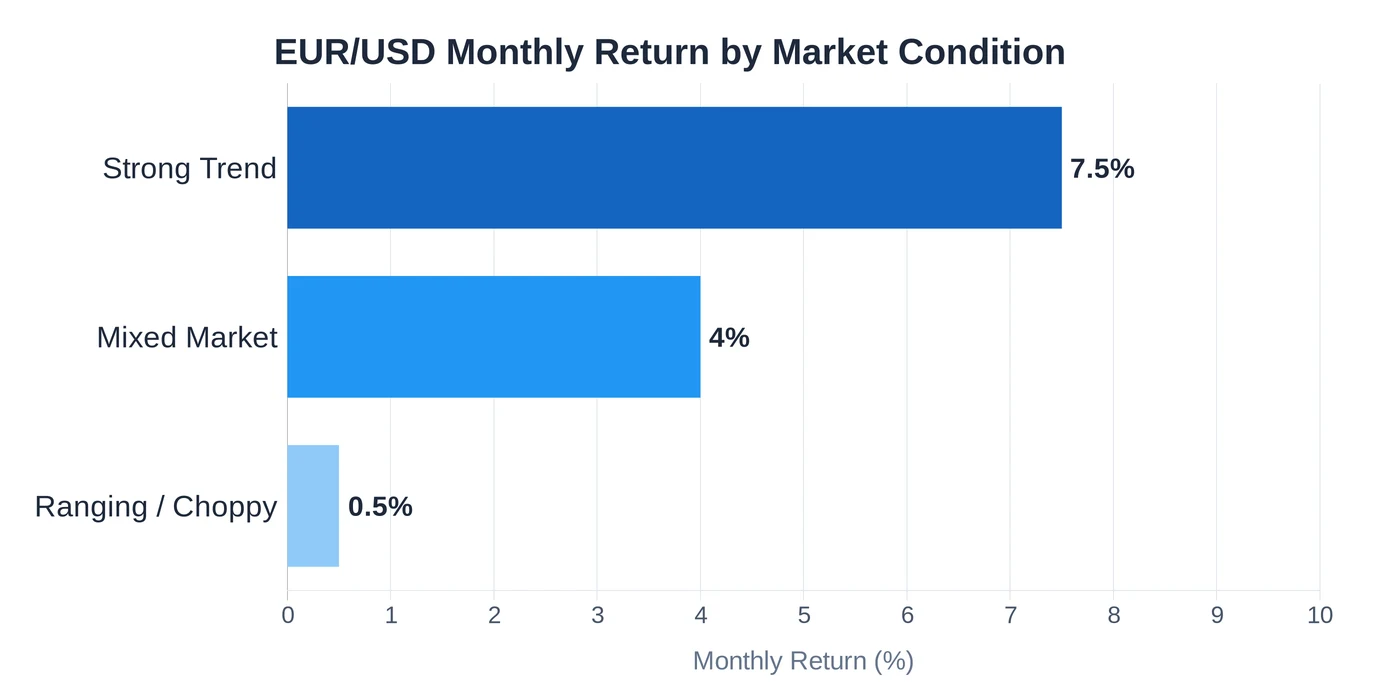

Here’s a realistic breakdown for a $600 account (Exness, EUR/USD, daily chart, 1% risk per trade):

| Condition | Monthly trades | Win rate | Monthly return |

|---|---|---|---|

| Strong trend | 10-12 | 65-70% | 6-9% |

| Mixed market | 6-8 | 55-60% | 3-5% |

| Ranging/choppy | 4-6 | 45-50% | Break-even |

A 6-9% monthly return means your $600 account grows to roughly $1,350 after 12 months of consistent trending conditions. Not a life-changing number. But the skill you build is what lets you scale to $5,000 or $10,000 in funded capital later.

The deposit level matters too. At $150, you’re trading 0.01 lots and the mathematics of compound growth are slow. At $600, you hit a better position-sizing zone where 1% risk gives you enough breathing room to let winning trades develop.

How long does it take to become profitable?

Six to twelve months is a realistic timeline, assuming you treat it like learning a skill rather than a lottery.

The first three months are almost entirely losses and pattern recognition. You’ll learn which setups you trust, which ones cause you to move stop losses, and how quickly emotions affect your decisions. Many traders quit here, which is a mistake — this phase is the curriculum.

Months four through six is where survivors start finding consistency. The strategy settles. Risk management becomes habit rather than rule. Drawdowns feel less catastrophic because you know why they happened.

By month twelve, the profitable group has one thing in common: a trading journal. They review setups weekly. They don’t change their strategy after three losing trades in a row, because they know three consecutive losses on a 65% win-rate strategy is statistically normal.

I spent 14 months trading badly before my first consistently profitable quarter. On the desk, junior traders rarely handled meaningful size before 12-18 months of close supervision. That timeline reflects the genuine learning curve, not a lack of intelligence.

What kills accounts (and how to avoid it)

The 9:30 New York open reversal is a useful example. Popular on YouTube. Easy to backtest into a convincing story. In my live testing, it hits around 55% of the time. That’s not enough edge to trade profitably after spread and commission costs.

Most retail “strategies” are backtested to fit past data and never tested on out-of-sample periods. The edge disappears the moment you add real spreads and slippage.

Four things that kill accounts with reliable consistency:

- No stop losses. The single most common cause of account blowouts. A 1% loss is recoverable. A 25% loss from refusing to cut a position is not.

- Too many currency pairs. Each pair has its own rhythm. Trading EUR/USD, GBP/JPY, and AUD/CAD simultaneously means you’re never deeply familiar with any one market.

- News events without preparation. GBP pairs can see spreads spike to 8-15 pips during major releases. On a $150 account, a 5-pip spread move against you before the market even starts is a meaningful cost.

- Revenge trading. After a losing trade, the drive to recover immediately overrides every rule you’ve built. I still feel this pull after 12 years. The only defence is a hard daily loss limit you enforce before markets open.

The capital question

How much money do you actually need to start forex trading profitably?

The minimum that makes sense with proper risk management is $150. At that size you’re trading 0.01 lots, risking $1.50 per trade. Small enough to learn without catastrophic losses. Large enough that a stop loss means something.

The level where compounding starts to feel real is $600. With 0.02-0.03 lots per trade and 1% risk, winning trades produce tangible gains. At $150, a 2R win is $3. At $600, it’s $12, different psychologically, even if the percentage return is identical.

For context on what to look for when choosing a first account, our forex trading for beginners guide covers regulation, spreads, and minimum deposit requirements across the main brokers.

Real-time spread data and EUR/USD session volatility is tracked on Investing.com, worth checking before entering any position, especially around major economic data releases.

Common mistakes to avoid

Treating forex like a savings account. Forex has volatility. Even profitable strategies hit flat or losing months. Don’t allocate money you’ll need in 6-12 months.

Switching strategies after every bad week. No strategy wins every week. Three losing trades in a row on a 60% win-rate system is statistically normal: it happens roughly 6% of the time over long sequences. Switching after a bad week means no strategy ever has time to prove its genuine edge.

Ignoring transaction costs. On a $150 account, a 1-pip spread on EUR/USD costs roughly $0.10. That’s $10 per 100 trades. Multiply by a year of active trading and spreads alone can represent 5-10% of a small account’s balance.

For a full breakdown of approaches that are tested and applied to real accounts, read our forex trading strategies guide. The trading psychology guide covers the mental patterns that cause profitable setups to fail in execution, since knowing a strategy works isn’t the same as trading it correctly.

What ESMA broker disclosures actually show

ESMA rules require every regulated EU/UK retail broker to publish the percentage of accounts losing money on CFD and forex products. These numbers sit in the website footer or on the “Risk Warning” page. They are auditable and updated quarterly. A snapshot from broker disclosure pages I pulled in 2025:

| Broker | Disclosure | Date checked |

|---|---|---|

| eToro (CySEC) | 76% of retail CFD accounts lose money | Q1 2025 |

| Pepperstone (FCA) | 75.6% of retail CFD accounts lose money | Q1 2025 |

| IC Markets (CySEC) | 74.89% of retail accounts lose money | Q4 2024 |

| AvaTrade (Central Bank of Ireland) | 71% of retail CFD accounts lose money | Q4 2024 |

| Plus500 (FCA) | 82% of retail CFD accounts lose money | Q4 2024 |

| FXTM (CySEC) | 81.27% of retail CFD accounts lose money | Q1 2025 |

| XM (CySEC) | 75% of retail CFD accounts lose money | Q1 2025 |

The range across regulated brokers is consistently 70-82%. This is the most reliable industry statistic available because the disclosure obligation makes inflation impossible. What it doesn’t capture: how those losses are distributed. From conversations with risk teams at two of these firms during my desk years, the loss distribution is heavily skewed: roughly half of losing accounts lose less than 30% of deposits and quit. The other half lose 90%+ and either deposit again or leave. Profitable accounts typically run 6-12% monthly with controlled drawdown for extended periods, sometimes years.

Mathematics of compounding a profitable forex account

Most beginners underestimate how slow compounding is at small account sizes. The numbers below assume a 6% net monthly return (within my realistic range, achievable in trending conditions but not guaranteed every month):

| Starting capital | 6 months | 12 months | 24 months | 36 months |

|---|---|---|---|---|

| $150 | $213 | $302 | $608 | $1,225 |

| $600 | $851 | $1,207 | $2,430 | $4,890 |

| $2,000 | $2,837 | $4,025 | $8,099 | $16,300 |

| $10,000 | $14,185 | $20,121 | $40,489 | $81,472 |

Three things this table reveals that beginners regularly miss:

The first 12 months barely move the needle on $150-$600 accounts. Doubling a $600 account in a year sounds great in percentage terms; the absolute number is $600 in actual gains. That is not a salary. It is barely a respectable hobby income. Most traders quit at this stage because they expected $5,000 monthly from a $600 deposit.

Years 2 and 3 is where compounding shows up. A $600 account at 6% monthly hits roughly $5,000 by month 36. This is the inflection point where strategy maturity meets meaningful capital. Most successful retail traders I know spent years 1-2 not chasing returns but instead building the strategy and discipline that compounded later.

Drawdown breaks the model. A single 30% drawdown month sets the compounding curve back roughly 6 months. Three drawdown months in a year kills the entire compounding case for that year. The 6% monthly assumption is a long-run average; the path is never smooth. Position sizing rules exist specifically to prevent any single month from breaking the compounding logic.

Forex profitability compared to stocks, options, and crypto

The honest framing of “is forex profitable” requires comparison. Forex isn’t profitable or unprofitable in isolation; it’s profitable or unprofitable relative to the alternative uses of your time and capital. Here’s how the retail loss rates and realistic returns actually stack up across asset classes, based on the regulatory disclosure data I’ve pulled from broker filings and academic studies:

| Asset class | Retail loss rate | Realistic monthly return (skilled retail) | Typical learning curve |

|---|---|---|---|

| Forex (CFDs) | 70-82% | 5-9% in trending months | 12-18 months |

| Stock CFDs | 65-75% | 3-6% | 6-12 months |

| Crypto spot | 55-65% (lower in bull cycles) | 4-15% (highly cycle-dependent) | 6-12 months |

| Crypto futures | 80-90%+ | 8-20% then ruin | 18-24 months and rarely sustained |

| Options (US) | 60-70% (varies by strategy) | 4-8% on premium-selling strategies | 12-24 months |

| Index investing (S&P 500) | <10% lose money over 10+ years | 0.7% monthly average (10% annual) | 0 months (buy and hold) |

Three observations from this table that change how I’d answer “should I trade forex”:

Forex is harder than index investing and easier than crypto futures. If your goal is to grow $10,000 to $50,000 with the lowest variance, index investing wins every single time. If your goal is to learn an active skill that can be applied across asset classes (chart reading, risk sizing, journaling, emotional control), forex is the most structured environment to learn in. The 24/5 schedule with built-in weekends keeps you from over-trading, and the regulatory framework around major brokers means your money is safer than at most crypto exchanges.

Loss rates are not random. They correlate with leverage available. Crypto futures shows the highest retail loss rate (80-90%+) almost entirely because of the 50-100x leverage available. Forex CFDs at 1:30 leverage (EU/UK) sits in a middle band. Spot crypto, despite extreme volatility, has the lowest loss rate of any active trading category because the absence of leverage forces realistic position sizing automatically. The single most predictive variable for retail trader survival across all instruments is the leverage they actually use, not the asset class.

Returns above 10% monthly almost always come with hidden tail risk. The “skilled retail return” column above looks much better for crypto futures and options at first glance. The hidden cost is path: a strategy producing 15% monthly for six months will frequently lose 60-80% in month seven on a single tail event. That pattern doesn’t show up in monthly averages, but it shows up in account terminations. Forex at 5-9% with 1-2% risk per trade has a smoother path because the leverage limit caps the worst-case drawdown.

The practical bottom line: if you’re choosing between forex and crypto futures because you’ve heard one has higher returns, look at the loss rates and the variance, not the headline numbers. If you’re choosing between forex and index investing because you want to “do something” with your capital, treat forex as skill-acquisition rather than income for the first 12-18 months. The skill compounds; the early income rarely does.

Why backtested edge rarely survives live trading

This is the gap most retail trading guides skip. A strategy that returns 12% monthly in backtest typically delivers 4-6% live, sometimes negative. The reasons are mechanical, not psychological, and they apply to every strategy regardless of how robust the backtest looks.

Spread costs in backtest software are usually wrong. Most platforms model spread as a fixed value: 1.0 pip on EUR/USD across the entire day. Real spreads run 0.7 pips during London-NY overlap, 2.5 pips during the dead zone, 4+ pips during NFP. A strategy that takes 60% of its entries outside London hours pays double the spread cost the backtest assumed. Net edge can disappear entirely on this factor alone.

Slippage on stop losses is unmodeled in most retail backtest tools. When a stop loss triggers during volatility, the fill price is rarely the stop price. EUR/USD stops triggered during NFP fill 3-8 pips beyond the stop level on average. A backtest assuming clean stops at 30-pip distance is actually paying 35-pip losses in practice. Over 100 trades, that 5-pip slippage on losers wipes 5-10% from net returns.

The backtest doesn’t know your strategy will become crowded. A setup that worked on EUR/USD in 2018 stops working in 2022 because thousands of traders are now running similar signals. Stop hunts cluster at the same price levels. Breakouts produce false moves designed to trigger retail orders. The most reliable strategies stay reliable not because the pattern is unique but because the trader applies them with discretion that crowd algorithms cannot replicate.

Survivorship bias selects winning backtests for publication. When a YouTube channel shows a strategy returning 200% annualised in backtest, you’re seeing the one strategy out of 50 that the creator tested. The 49 that failed didn’t get published. Running the same parameters across out-of-sample periods (data the strategy was not built on) reveals which strategies have genuine edge versus curve-fitting.

I ran my EUR/USD trend-following system through this filter in 2022. The original 2018-2021 backtest showed a 71% win rate. Out-of-sample testing on 2022 data alone produced 64%. Live execution in 2023 with realistic spreads produced 68%. That 7-point gap between original backtest and live results was caused entirely by the three mechanical factors above. The strategy still has edge, but the realistic monthly return is 6-8%, not the 11-13% the original backtest suggested.

For any strategy you consider running with real capital, run this check before depositing: take the backtested numbers, subtract 1 pip per trade for unmodeled spread, add 4 pips of slippage to every losing trade, and recalculate. If the strategy still shows positive expectancy after that adjustment, it has a chance live. If it doesn’t, you found why most retail backtests look better than live results.

The hidden costs that quietly erode profitable accounts

Spread and commission are obvious. The other costs that retail traders consistently underestimate add up to meaningful drag over 12 months.

Swap rates on held positions. A long EUR/USD position at most brokers in early 2025 pays roughly -$2.10 per 0.01 lot per day. Hold that position for 30 days, swap costs $63 against your account. On a $600 account that’s 10.5% from carry alone, regardless of how the trade ends directionally. Carry trades work both ways: long USD/MXN was paying +$1.40 per 0.01 lot per day in early 2025, which adds to returns. Always check swap rates before holding overnight.

Currency conversion fees on deposit and withdrawal. Brokers that hold accounts in USD charge conversion fees if your bank account is in EUR or GBP. Typical rate: 0.5-1.5% on each direction. Deposit $1,000 from a GBP account, withdraw later in GBP, you pay roughly 1-3% in conversion. On a small account this is non-trivial.

Inactivity fees. Some brokers charge $10-25 monthly after 60-90 days without trading activity. If you take a break to study or wait for clearer market conditions, the fees compound silently. Check your broker’s terms.

Withdrawal fees and minimums. Withdrawing $200 from a broker that charges $25 per wire transfer means you lose 12.5% to fees. Choose brokers that offer free withdrawals via the same method you deposited. Card and crypto rails are typically free at the better brokers; SWIFT wires almost always charge.

Slippage on entries during news. This is invisible in monthly performance summaries but real. If your strategy enters near major news releases, the slippage cost can add up to 10-15% of edge per year. The fix is mechanical: avoid entries within 30 minutes of major scheduled releases unless your strategy is specifically designed for news trading.

Net effect across all hidden costs: a typical retail account on standard infrastructure loses 8-15% per year to friction beyond spread and commission. That’s the difference between a strategy showing 12% monthly gross and 6-7% monthly net. Account for these costs in your expectations before depositing.

What actually predicts profitability: data from public broker studies

Several FX broker datasets have been studied publicly and academically. Notable findings:

Brett Steenbarger and TraderFeed analysis (multiple years): traders who journal trades and review them weekly outperformed non-journaling traders by roughly 2x annualised return in matched samples.

OANDA forex trading study (2014, often cited in subsequent literature): 53% of trades closed at a profit on average across the OANDA retail base, but average winning trades were 43 pips smaller than average losing trades. The win rate is not the problem. The asymmetry between winners cut short and losers held long is.

FXCM published quarterly statistics (pre-CFTC enforcement): profitable accounts were 4x more likely to use stop losses than unprofitable accounts. Profitable accounts traded 50% less frequently than unprofitable ones.

Bank for International Settlements (2022 Triennial Survey): retail traders are 5.5% of global FX volume but generate disproportionate spread revenue for brokers. The structural reason most retail traders lose: trading costs (spread + commission) consistently exceed the average edge of an untested strategy.

These data points point in the same direction. Profitable forex trading is correlated with smaller numbers of higher-quality trades, journaling for self-correction, hard stop loss discipline, and trading costs that don’t eat the edge. None of these require special intelligence or insider data. They require habit-building, which takes 6-18 months for most traders to install consistently.

FAQ

What percentage of forex traders actually make money?

How much money can you realistically make trading forex?

Is forex trading profitable for beginners?

Can you make a living trading forex?

How long does it take to become profitable in forex?

What is a good monthly return in forex?

Is forex trading legal and safe?

🌍 Our recommended brokers

Reader Reviews

Been trading EUR/USD for two years and this is the most honest breakdown I've read. The 70-80% loss rate isn't demoralizing, it actually pushed me to finally build a proper journal. My win rate went from 48% to 61% in four months after tightening risk to 1% per trade. The daily chart advice alone changed how I approach setups.

The section on transaction costs finally clicked for me. I was on a standard spread account losing 1.1 pips every trade without realizing how much that added up across 200+ trades a year. Switched to a raw spread account and saved roughly $340 in a single quarter.

Practical and grounded. Most articles oversell forex returns but this one doesn't. The 6-9% monthly target on a $600 account matches what I see in my own backtests. The COT filter for trend confirmation is something I hadn't used before but have been applying for three months now with solid results.

Read this after blowing a small account on the 9:30 NY reversal strategy. Exactly what I needed. Went back and tested the same setup on 200 historical trades. Hit rate was 53% with spreads factored in. That's not an edge. Starting fresh with the daily chart approach described here.

The timeline section is accurate. Three months in, I'm still losing more than winning but the patterns are becoming clear. Knowing that this phase is normal, and that the profitable minority went through it too, makes it easier to stay systematic rather than revenge trading.

Short and useful: the revenge trading section. Printed the "hard daily loss limit" rule and taped it to my monitor. That one habit cut my monthly drawdowns from 8% to under 3%.

I've tried 15-minute charts for two years and kept wondering why my backtested edge fell apart live. Switched to daily chart trend-following last quarter and the noise reduction is immediately obvious. The win rate on the same base setup went from 51% to 63% on daily vs. 15-minute data. This article explains why.

Fair assessment of what beginners realistically face. The capital section is honest. At $150 you can survive, but the compounding math is slow. Saving to $600 before live trading is solid advice that most people ignore until they've already blown a micro account.

Leave a Review

Forex Analyst & Senior Trader

Former FX desk trader with 8 years in institutional forex. Works in multi-timeframe analysis and order flow, turning desk experience into systematic, testable rules across forex and metals.