When forex market hours actually move, in one chart

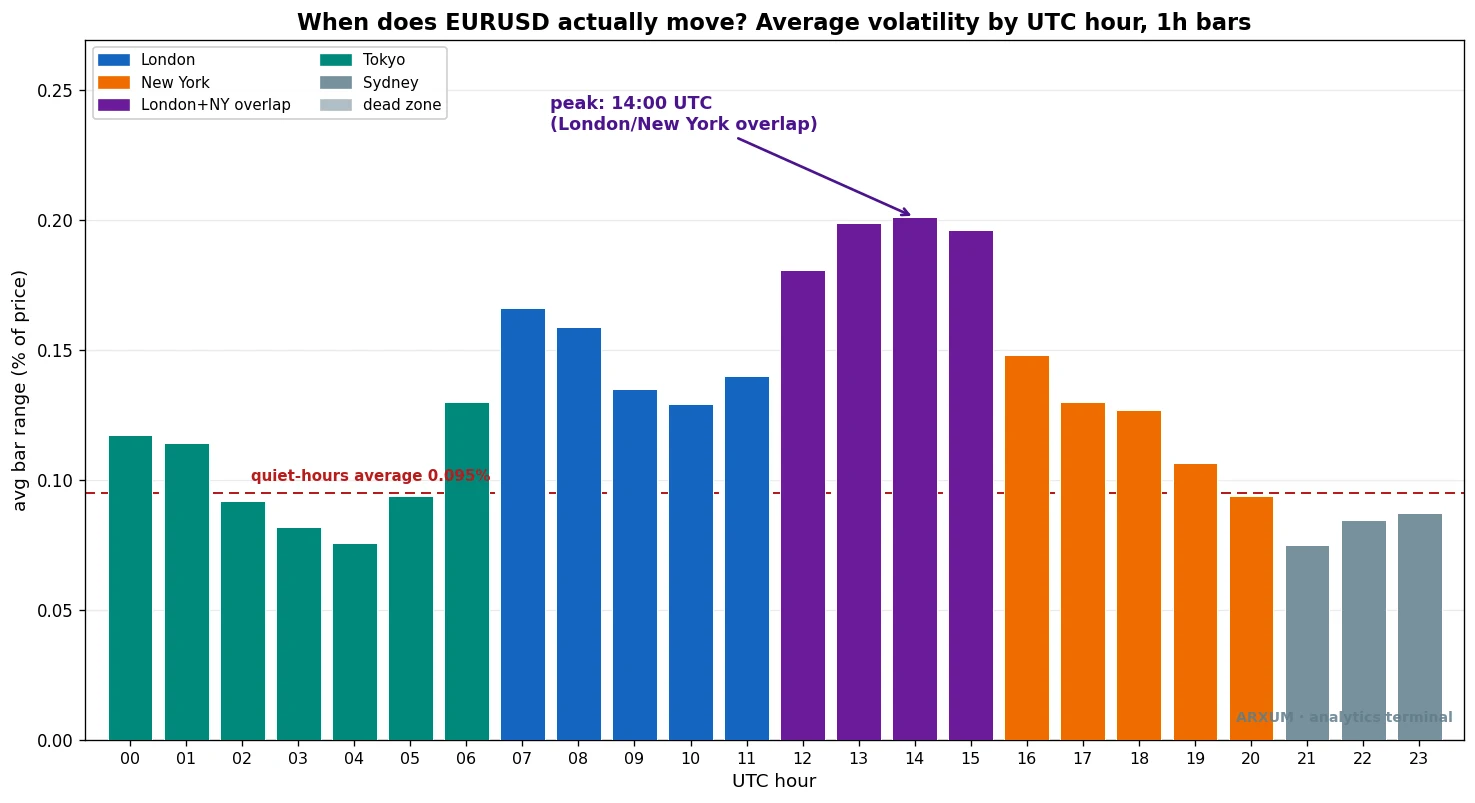

Here is the thing you came for, straight away. This is the average size of a one-hour candle on EUR/USD, hour by hour in UTC.

We measured it across the last year and a half of real data. Taller bars mean price moved more in that hour.

The shape tells the whole story. Price sleeps through the small hours, then wakes up when London opens near 07:00 UTC.

It hits its loudest point at 14:00 UTC, when London and New York are both open at once. After New York’s afternoon it fades away again.

The dashed line marks the quiet-hours average of about 0.095%. Bars below it are the sleepy hours, and bars well above it are where the money is made and lost.

That single peak at the overlap is the answer most people are searching for. Trade in the tall bars and price moves with purpose.

Trade in the short ones and you are paying a spread to watch a flat line.

The rule of thumb: the busiest, cleanest forex hours are the London-New York overlap, roughly 12:00-16:00 UTC. The quietest are the pre-London hours from about 21:00 to 05:00 UTC.

The four forex trading sessions

The market is usually carved into four sessions, each named after a major financial center. As one closes, the next is already open, so there is never a true gap.

Here is how they line up in UTC, the clock most trading platforms default to.

| Session | UTC open | UTC close | Pairs that move most | Typical activity |

|---|---|---|---|---|

| Sydney | 21:00 | 06:00 | AUD/USD, NZD/USD | Low |

| Tokyo | 00:00 | 09:00 | USD/JPY, EUR/JPY | Moderate |

| London | 07:00 | 16:00 | EUR/USD, GBP/USD | High |

| New York | 12:00 | 21:00 | EUR/USD, USD/CAD, XAU/USD | High |

A quick word on each, because the pair you trade should follow the session you trade in.

Sydney is the quietest. The Australian and New Zealand dollars move best here.

A EUR/USD strategy run during Sydney hours tends to underperform, not because it is a bad strategy, but because it is in the wrong liquidity.

Tokyo brings the yen crosses to life. USD/JPY often shows its cleanest trends in Asian hours.

EUR/USD tends to drift in a range here rather than trend, which quietly frustrates breakout traders.

London is where forex comes alive. The UK handles the largest slice of global forex turnover.

The first couple of hours after the London open are among the most active of the day for both GBP/USD and EUR/USD.

New York adds US dollar volume and the second-biggest center by turnover. The US morning is where dollar pairs and gold get their second wind, and the overlap with London is the high point.

Notice something in the data above. The four sessions already cover all 24 hours with overlap, so there is no literal dead hour with zero session.

When traders say “dead zone,” they mean the low-activity single-session hours before London, not a gap on the clock.

Every instrument peaks at the same hour

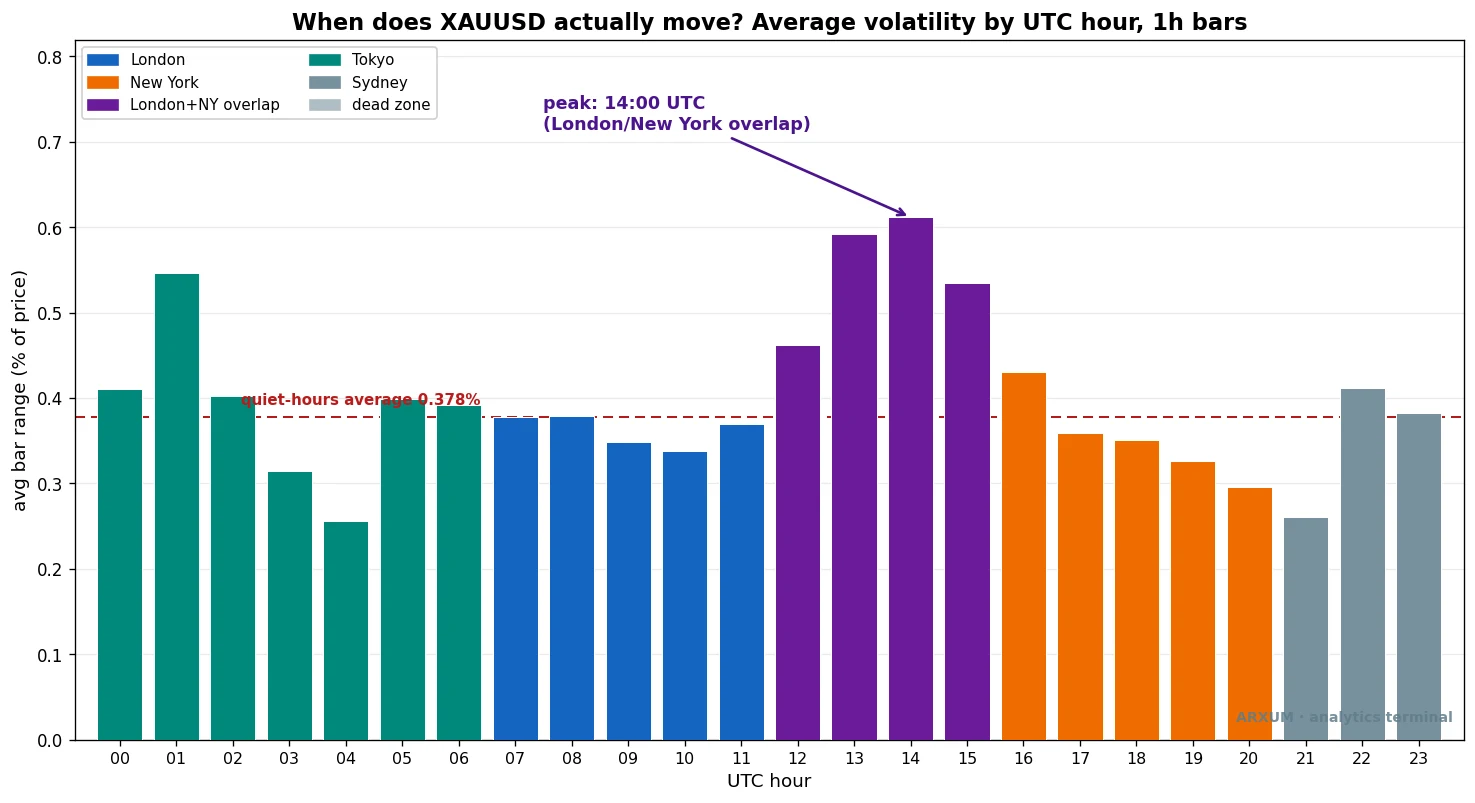

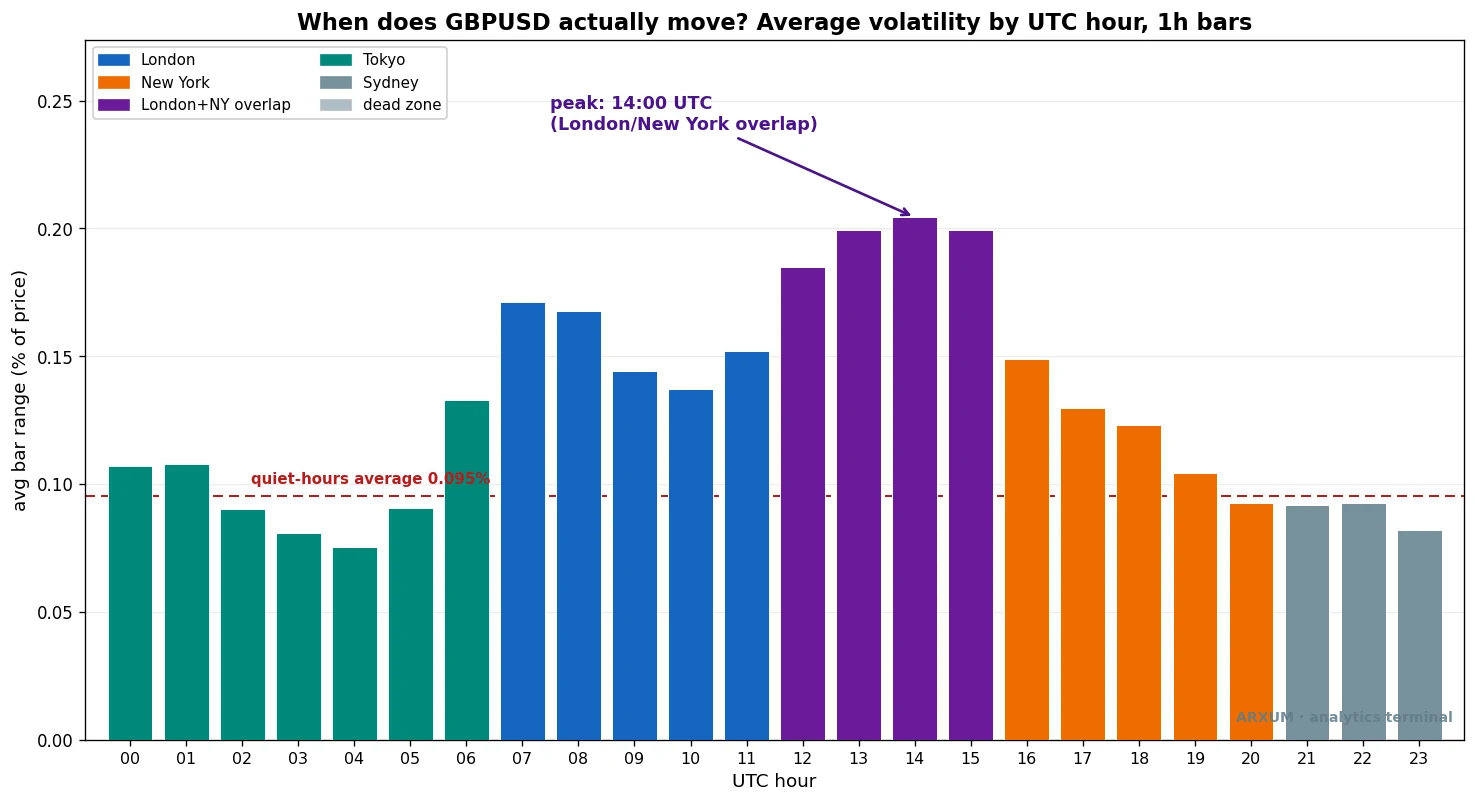

One pair could be a coincidence. So we ran the same measurement on spot gold (XAU/USD) and on GBP/USD over the same window.

The result is almost eerie: the exact same shape, and the exact same 14:00 UTC peak.

Gold moves in far bigger percentage swings than a major pair, so its bars tower over EUR/USD’s in absolute terms. But the rhythm is identical: quiet in Asia, building through the London morning, loudest at the overlap.

The pound tracks the euro closely, which makes sense. Both are London-anchored, and both live for the London morning and the overlap.

Three different instruments, three different scales, one shared clock. This is the safe, universal takeaway of the whole piece, and it holds no matter what setup you layer on top of it.

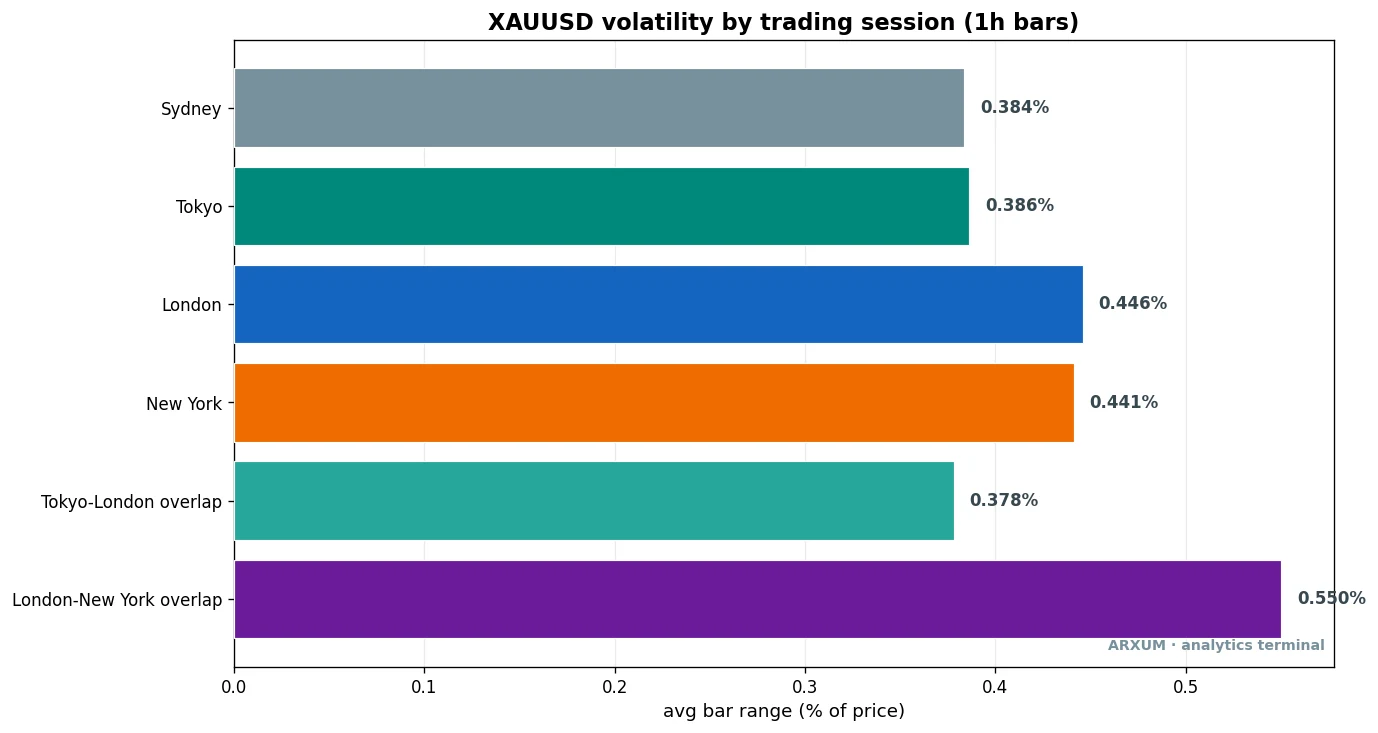

The overlap, session by session

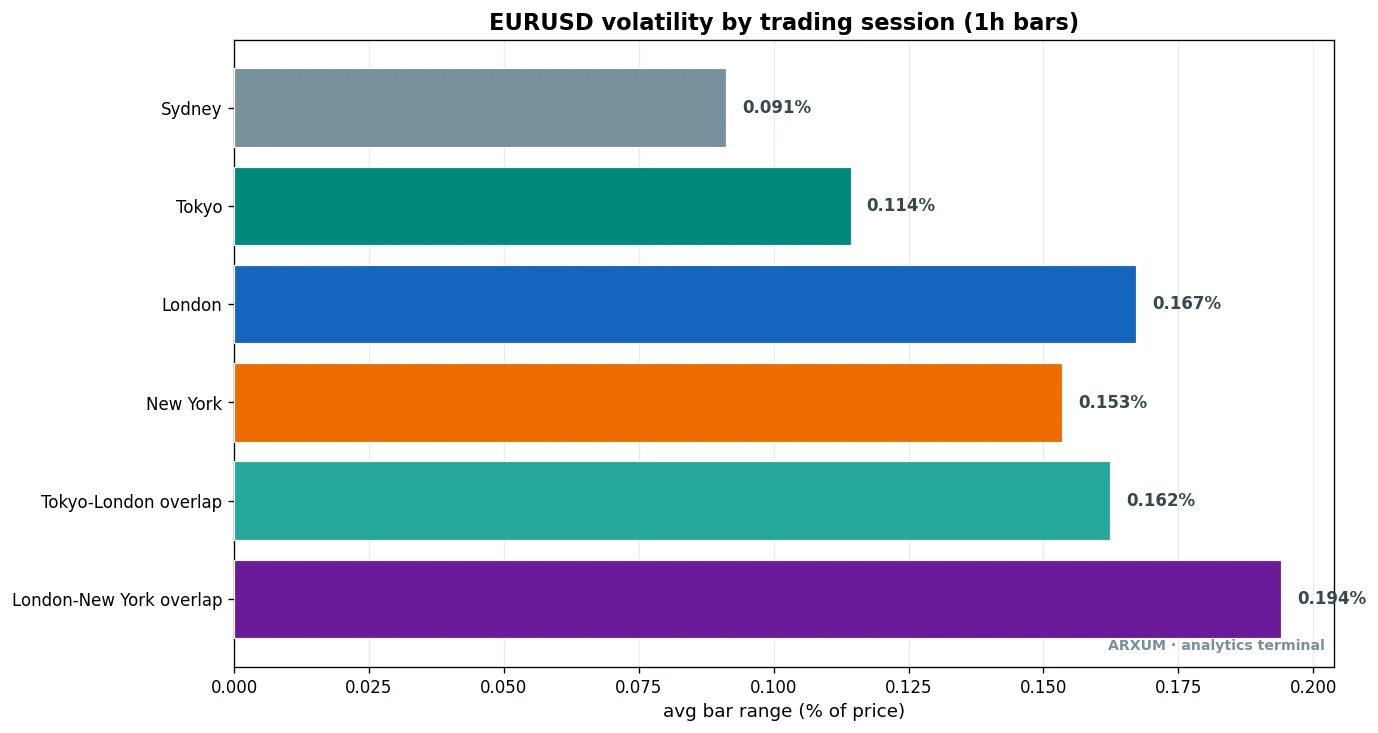

Averaging by hour is one view. Averaging by the named session is another, and it settles the “which session is busiest” argument directly.

Here is EUR/USD’s average one-hour range grouped by session.

The overlap runs about twice as active as Sydney. London on its own edges out New York on its own, and the Tokyo-London handover in the mid-morning is a respectable third.

Gold sorts the same way.

The takeaway for pair selection: if you can only trade one window, trade the overlap, and trade the London-anchored instruments (EUR/USD, GBP/USD, gold) in it.

If your hours land in the Asian sessions, switch to the yen crosses and the Aussie. That is where the liquidity actually is at that time.

Forcing EUR/USD into Tokyo hours is trading in the wrong ocean.

Now match that to your own clock, which is the single most useful thing to do before you trade a thing. The overlap runs 12:00-16:00 UTC, so convert it to where you live:

- US East Coast (UTC minus 5): the overlap is your 07:00-11:00, a workable pre-work or early-morning window.

- UK and Western Europe (UTC to UTC plus 1): it lands over your lunch and early afternoon, the easiest fit of all.

- Asia-Pacific (UTC plus 7 to plus 10): the overlap falls in your evening, so trade it after work. Or trade the yen crosses in your own morning during Tokyo hours instead.

Pick the window your life actually allows first, then choose the instrument that moves in it. A setup that fires at a time you cannot be at the screen is not a setup you can trade.

Can you trade the clock itself?

Knowing when the market moves is useful on its own. But it raises an obvious question.

If 07:00 UTC reliably wakes the market up, can you trade the London open directly, with a mechanical rule and no discretion?

There is a classic setup for exactly this, the London opening-range breakout. It is simple enough to state in one breath, which is why it is worth testing rather than trusting.

The rules fit on a napkin:

- The box: the high and the low of the first hour after the London open.

- Long: buy if price closes above the box high.

- Short: sell if price closes below the box low.

- Stop: the opposite edge of the box.

You are betting that the first real move out of the opening range is the move that sticks.

Here is that idea on a real recent EUR/USD chart, so you can see the pieces before we test whether it pays.

Walk the chart left to right. The blue shaded box is the London opening range, the first hour after the 07:00 UTC open.

The dashed blue line is its ceiling, the dashed red line its floor.

Price closed above the ceiling, and that green arrow is the entry: buy the close above the range high. The stop went on the box floor, shown in the ticket: entry 1.0698, stop 1.0629.

That gap from entry to stop is your risk.

Price then walked up over the next day to 1.0834, a gain of about +1.3%, twice the risk. That is a reward-to-risk of 1:2: the trade made back twice what it put at stake.

We write every payoff that way here. The 1 is the risk from entry to stop, and the X is the reward as a multiple of it.

Two more pieces on the chart matter, and both are filters we explain properly below. The vertical dashed line marks the entry bar so you can line it up across both panels.

The solid blue line is a fast moving average sitting above a slower dashed one. That is the note in the corner: intraday uptrend, longs only.

And the tall volume bar under the entry is the note “volume 1.7x average.” Hold those two thoughts.

They turn out to be the difference between a real edge and a coin flip.

The raw version barely works

The honest starting point: buying every London breakout, with no filter at all, is close to a break-even trade. Here is the raw EUR/USD result on the long side, taking every qualifying close above the box over the recent 1.5-year window, fees included.

| Trades | 227 |

| Win rate | 41% |

| Reward-to-risk | 1:1.6 |

| Profit factor | 1.08 |

| Net return on $1,000 | +2.5% |

Two terms this table leans on. Profit factor is the whole strategy’s total winnings divided by its total losses, so anything above 1.0 is profitable.

A reading of 1.08 means you won about $1.08 for every $1 you lost. That is thin.

Win rate is just the share of trades that made money, 41% here. So you lose more often than you win and rely on the winners being bigger.

A profit factor of 1.08 is the kind of edge that slippage and a wide spread can quietly erase. The reason is the same one that dooms most raw breakout systems.

With no filter you take every breakout, including the limp ones that nudge over the line on no participation and roll straight back.

We needed a way to tell a breakout that means it from one that is just stretching its legs. And here is the useful part, the one that keeps this from being a fixed recipe.

The filter that works is not the same on every instrument.

What the sweep actually rewarded

We did not assume a filter. We swept a wide menu across each instrument, one condition at a time, and kept only what the data paid for.

The menu included volume, an intraday trend gate, a longer-term trend regime, a volatility filter, a trend-strength gauge, and a couple of momentum filters. Two winners emerged, and they were different for each market.

On EUR/USD, the filter that paid was volume. Only take the breakout when the breakout bar’s volume is at least 1.5 times its recent average.

| Filter | Trades | Win rate | Profit factor |

|---|---|---|---|

| No filter | 227 | 41% | 1.08 |

| Volume above 1.5x | 107 | 50% | 1.41 |

| Intraday trend gate | 110 | 43% | 1.18 |

| Volume plus trend gate | 50 | 52% | 1.40 |

The volume filter is the one that moves the needle, from a marginal 1.08 to a real 1.41. Adding the trend gate on top does not improve it, which is worth saying out loud: more rules is not more edge.

The plain volume filter, on its own, is the version to trade.

Why volume, and how to read it. Volume is simply how much trading happened on a bar, drawn as the histogram under the price.

A real breakout is crowded, with plenty of orders hitting at once, so its bar towers over the recent average. A fake one drifts across the line on thin air.

Most charting tools show this the instant you add a volume moving average set to 20 bars. If the breakout bar is clearly taller than that average line, roughly 1.5 times or more, it qualifies.

One honest wrinkle for forex, which we come back to at the end. Currencies have no central volume tape, so what you get is tick volume, a count of how often the price updated.

It is a proxy, and on this data it did its job.

Here is the proof the filter is doing something real, not just getting lucky. The breakouts it threw away, the quiet ones, should be clearly worse than the ones it kept.

They are: the low-volume breakouts we skipped ran at a profit factor near 1.0, dead money, while the high-volume ones we took ran at 1.41. That gap is the filter separating conviction from noise.

A winning EUR/USD trade, start to finish

Numbers settle the argument; a chart shows you the trade. Here is a clean EUR/USD long that the filtered rules took.

Price spent the London morning coiled in a tight opening-range box near 1.10. The breakout bar closed above the ceiling on volume about 1.2 times average.

The fast moving average was above the slow one, so the intraday trend was up and longs were on.

Entry was 1.1037 on that close, the stop went on the box floor at 1.0967, and the target sat twice that risk away.

- Entry: 1.1037, on the close above the range high.

- Stop: 1.0967, the box floor, your 1.

- Exit: 1.1178 about six hours later, a +1.2% gain at 1:2.

Six hours, in and out inside the same session. That is the discipline of this setup: it is a day trade, never carried past the London close.

An overnight surprise can never turn a small winner into a large loser.

When it fails, and why we show you

A filter improves your odds. It does not buy certainty.

Here is a EUR/USD breakout that cleared the filter cleanly and still lost.

This one had everything the rules ask for. Price broke the box high at 1.1427, volume was a loud 2.0 times average, the trend was up.

It went in, stalled, rolled over, and hit the stop at 1.1284 about eight hours later. A full loss, held near the 1 you risked by the box-floor stop.

That is the honest shape of this setup, and of every breakout method. You lose more often than you win, and the math only works because the losers stay small and the winners run bigger.

A 41% win rate on the raw version, closer to 50% with the filter, means losing streaks are normal, not a sign the method is broken.

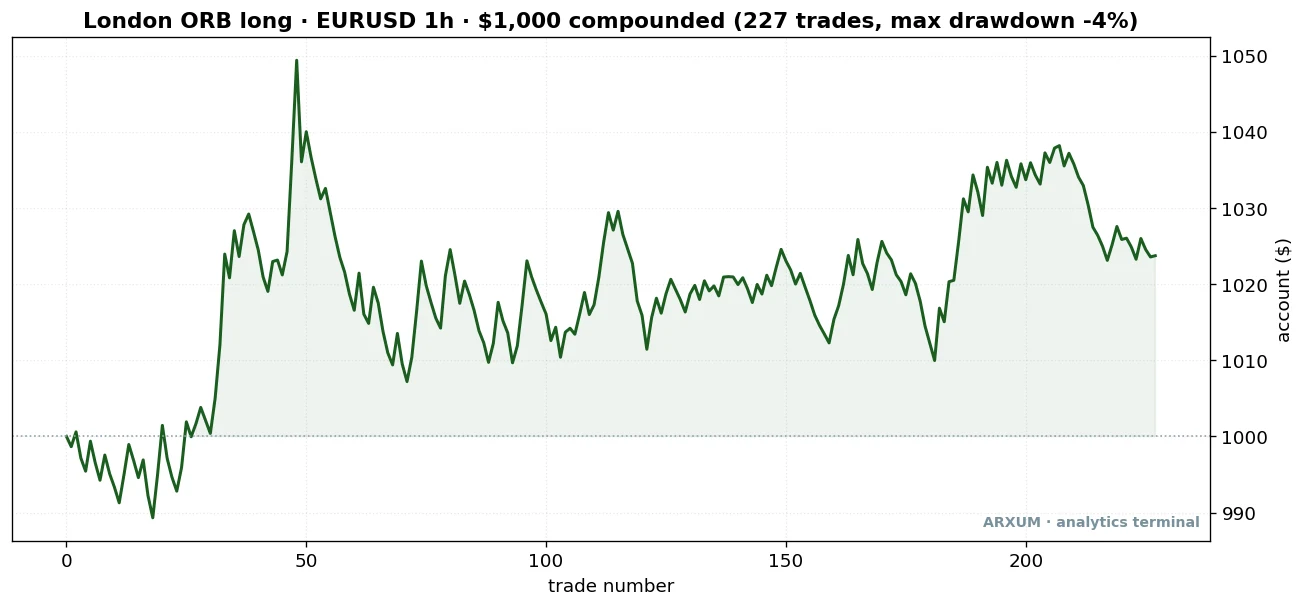

The real record, not two lucky trades

Two example charts prove nothing on their own. What matters is what the filtered setup did over the whole window.

Here is the equity curve: a $1,000 account run through every filtered EUR/USD trade in order, compounding as it goes.

Read the shape, not just the endpoint. This is what the volume-filtered London breakout on EUR/USD did over about a year and a half.

A jagged grind, an early dip below the starting line, then a slow climb to roughly $1,054. It is not a smooth escalator.

It bleeds through small losers, then makes it back through a cluster of winners, over and over. The whole ride never fell more than about 2% below its peak.

That is a shallow drawdown, which just means the account never dug itself into a deep hole.

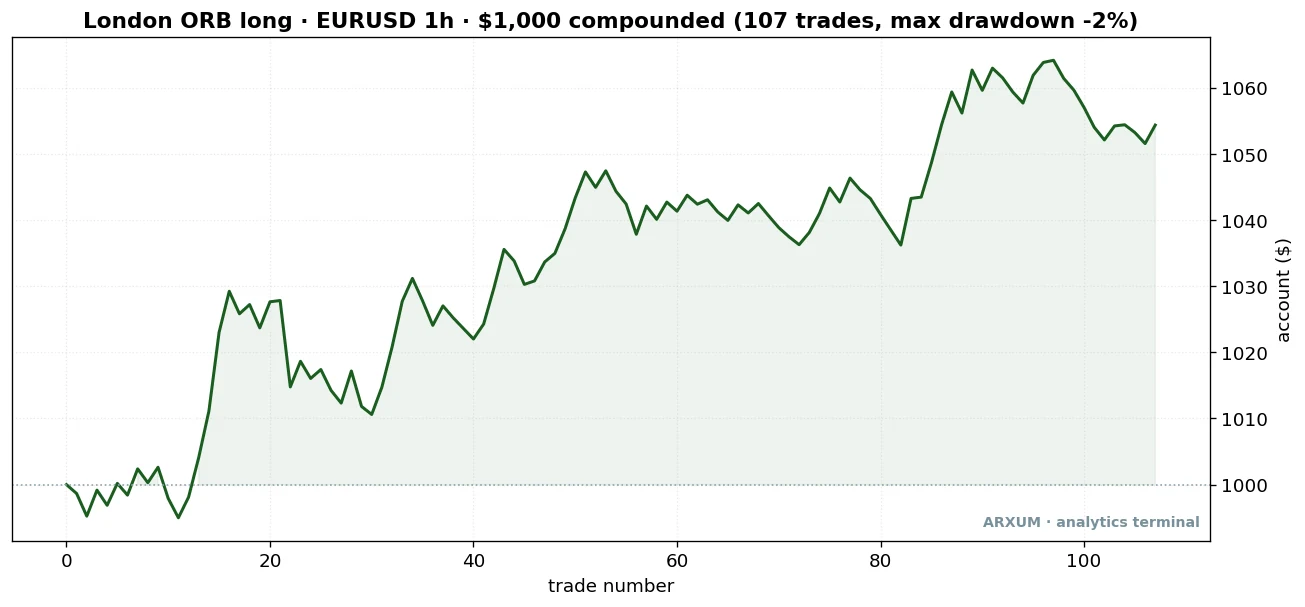

| Trades | 107 |

| Win rate | 49.5% |

| Reward-to-risk | 1:1.4 |

| Profit factor | 1.41 |

| Net return on $1,000 | +5.4% |

One number in that table can trip you up. The reward-to-risk reads 1:1.4, lower than the clean 1:2 on the single trades above, and lower than the raw version’s 1:1.6.

That is not a downgrade.

It is an average across every trade, winners and losers. The filter’s real gain shows up elsewhere: the win rate climbs to about 50% and the profit factor reaches 1.41.

A setup can make more money with a smaller average reward simply by being right more often.

Modest, and honestly so. This is one setup, on one side, on one instrument, and the volume filter cuts most signals.

That is why the trade count is around a hundred.

A real trader would run it alongside other setups and pairs, not as their only trade. The point is that a plain timing rule, filtered properly, produced a real, positive, verifiable record.

One caveat we will not bury. We split the window in half to check the edge is stable. On the earlier half the volume filter ran at a profit factor of about 1.15; on the later half it slipped to almost exactly 1.0.

In plain terms, the edge on EUR/USD softened in the more recent stretch. That does not make it fake.

But it means you should size it conservatively and watch whether it keeps paying, rather than assume the past year and a half repeats.

Gold trades the same clock, but the other side

Here is where the “one recipe” myth dies for good. On gold, the London breakout also pays, but not on the long side and not with the volume filter.

Gold rewarded the short side, gated by the intraday trend.

That word “gate” deserves a plain definition, since it is gold’s whole edge. The gate is a pair of moving averages, a fast one and a slow one.

A moving average is just the average price over the last several bars, a line that smooths out the jitter.

When the fast average is below the slow one, the short-term drift is down, so we take sell breakouts only. When it is above, we take buys only.

It keeps you trading with the immediate current, not against it. On gold’s chart the note reads “intraday downtrend, shorts only,” and that gate is what turned a losing raw setup into a winning one.

| Variant | Trades | Win rate | Profit factor |

|---|---|---|---|

| Short, no filter | 235 | 32% | 0.95 |

| Short, trend gate | 99 | 37% | 1.18 |

| Long, volume filter | 51 | 37% | 0.80 |

Look at that bottom row. On gold, the volume filter that saved EUR/USD actually hurts, dragging the profit factor to 0.80, a loser.

The edge here is the trend gate on the short side instead.

This is the whole reason the sweep matters: the filter is discovered per market, never assumed. What rescues one instrument sinks another.

Here is a gold short that worked, so the “sell the breakout” idea is not just a table. One note on the prices before you flinch at them.

This is spot gold, the live cash price of an ounce quoted against the dollar as XAU/USD. Gold’s recent bull run has carried that price into the high $4,000s per ounce.

The numbers below are real levels from the current market, not a typo.

Price closed below the opening-range floor while the fast average sat under the slow one, so the intraday trend was down and shorts were on. The green arrow marks the entry, sell the close below the range low, at $4,854.

The stop went on the box ceiling at $4,940, and price fell to $4,682 over the next fourteen hours, a +3.6% gain at 1:2.

And the honest other half, a gold short that failed.

The setup was clean: a close below the box at $4,070, the trend down, decent volume. Then price found a floor, turned, and climbed back through the stop at $4,156, a full loss over about a day.

Gold’s whole two-year backdrop was a powerful bull run, so shorting it was always fighting the bigger tide. That is exactly why some of these shorts get run over.

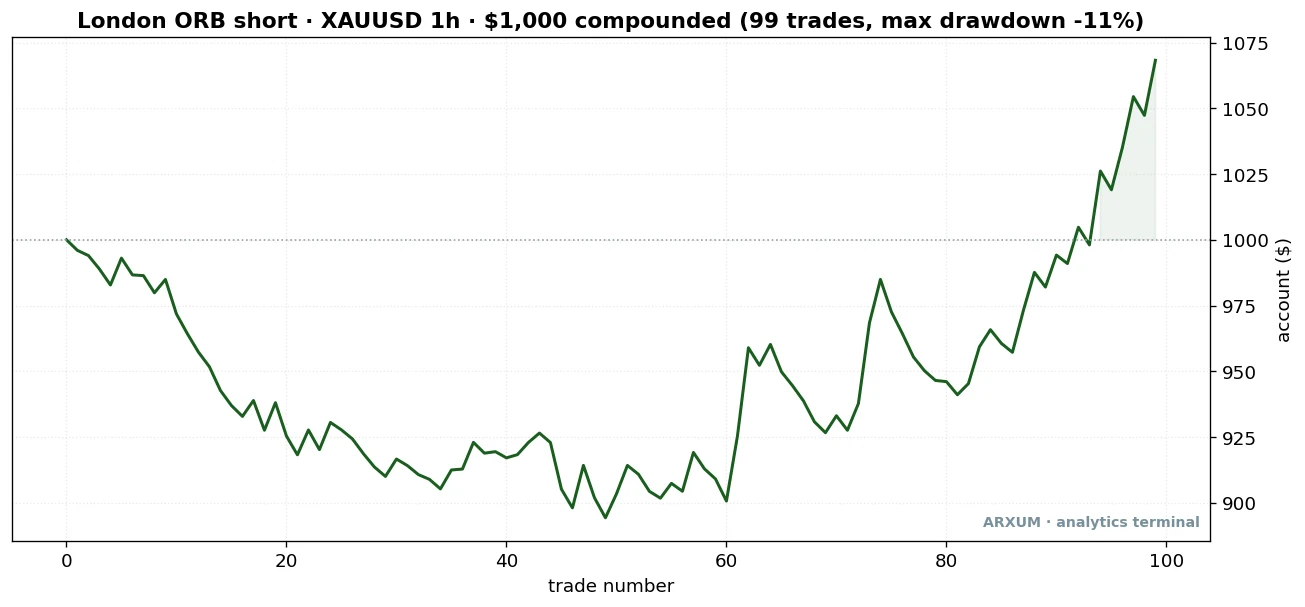

That tension shows up in gold’s equity curve, and it is the most honest chart in the piece.

This curve does something unusual and worth flagging. It spends the middle of the run losing, digging down to roughly $900, before recovering hard to about $1,068 by the end.

The account drawdown along the way reached about 11%, far deeper than EUR/USD’s. That is only the closed-trade view: at its worst moment the open short sat roughly 25% underwater before it came back.

When we split gold’s window in half, the halves disagreed sharply. The setup lost in the earlier stretch and won in the later one, the reverse of how edges usually behave.

| Trades | 99 |

| Win rate | 37.4% |

| Reward-to-risk | 1:2.0 |

| Profit factor | 1.18 |

| Net return on $1,000 | +7.2% |

The full-window profit factor of 1.18 is real and reported straight. But the two halves not agreeing is a caution flag: gold’s edge here is not stable across time.

So treat it as a lower-conviction setup than the number alone suggests, and size it small.

We would rather tell you that than sell you a clean story the data does not support.

The pound: an honest miss

We ran the exact same London breakout on GBP/USD, both sides, every filter. It does not pay.

Every reliable variant came out at break-even or a loss over this window.

| Variant | Trades | Win rate | Profit factor |

|---|---|---|---|

| Long, no filter | 244 | 37% | 0.85 |

| Long, momentum filter | 204 | 41% | 1.04 |

| Short, no filter | 223 | 34% | 0.83 |

One filter did clear a higher profit factor on the pound, but only across 37 trades. That is below the 50-trade floor we hold every setup to before calling it an edge, so we are not presenting it as one.

It is a thin lead worth a longer look someday, nothing you should trade on today.

This is the useful honesty. The pound is a fine instrument to trade the sessions with, since its own volatility-by-hour chart peaks at 14:00 UTC exactly like the others.

It is just not a place where this particular mechanical timing setup earned its keep over this window.

A method that works on two of three markets and admits the third is worth more than one that claims to work everywhere.

Reading the direction: which side, and when

The gold-versus-EUR/USD split is the real lesson of the mechanical setup, so it is worth stating as a rule you can carry to any market.

- Trade with the immediate trend, not against it. The intraday gate, that pair of moving averages, tells you the current drift. Fast above slow, take longs only. Fast below slow, take shorts only.

- The paying side is regime-dependent. Over this window, EUR/USD’s persistent grind higher meant longs paid and shorts lost completely. Gold’s backdrop meant the trend-gated shorts were the ones that worked. Neither is a permanent law; both are what the recent regime rewarded.

- If the trend flips, the paying side flips with it. These are not “gold is always a short” or “EUR/USD is always a long” rules. They are “trade the side the current regime is handing you” rules instead.

This is why the volatility clock and the mechanical setup are two different layers. The clock (when the market moves) is stable and universal.

The setup (which breakout to take) shifts with the market and needs the filter to find its footing.

What this costs you, and staying level-headed

A working setup and a blown account can start from the same rules. The gap between them is risk discipline, and it is short and specific here, tied to this setup’s real numbers, not a generic warning.

Risk a small, fixed slice per trade, around 2%. The filtered EUR/USD version wins about half its trades; the gold short wins closer to a third. Either way, losing streaks are normal, and your only job is to survive the cold stretches.

On a $1,000 account, 2% is $20 at stake per trade, and the placement steps below turn that $20 into an exact position size. Keep it that small and no single loser can bruise the account.

Expect the streaks, and do not chase. An edge that wins fewer than half its trades will hand you three, four, five losers in a row. That is variance, not failure.

The steady discipline is the whole game. Do not widen a stop to avoid taking a loss, and do not double up to win it back.

And do not turn euphoric after a big winner and oversize the next one.

Follow the plan through the boring middle, because the equity curves above show the middle is mostly boring.

Check live against the test, calmly. Say you trade this and it runs materially worse than these numbers over a real sample. That is a signal to step back and look at conditions, not to panic.

One bad week is noise. A sustained gap over many trades is the market telling you the regime has shifted, exactly what the EUR/USD half-split hinted at.

The honest read is somewhere between “ignore it” and “quit in a huff.” Watch it, size down when it wobbles, and only trade money you can afford to lose while you find out whether it fits you.

How to place one trade, step by step

Enough theory. Here is how a beginner actually places a London ORB long on EUR/USD, click by click, sized for a small account.

-

Set your chart to UTC and mark the box. On a 1-hour EUR/USD chart, find the first candle after 07:00 UTC. The high and low of that first hour are your box ceiling and floor. Most platforms let you add a session-highlighter overlay; TradingView has one free, and it draws the London window for you.

-

Wait for the close and check volume. You want a candle that closes above the box ceiling with volume clearly above its 20-bar average, about 1.5 times or more. Add a volume moving average set to 20. Eyeball whether the breakout bar towers over it.

-

Place a buy-stop, not a market order. Set a buy-stop order a touch above the box high, so you are filled only if price actually breaks out. In the stop-loss field, enter the box floor. In the take-profit field, enter a level twice the entry-to-stop distance away, your 1:2 target.

-

Size it to 2% risk. To size trades properly you need two words first. A pip is the smallest standard price step on a currency pair, the fourth decimal, so each 0.0001 of price is one pip. A lot is the size of your position. A standard lot is worth about $10 per pip on EUR/USD, and a micro-lot is a hundredth of that. Now work it from the account down, one step at a time:

- Risk budget: 2% of a $1,000 account is $20 at stake.

- Stop distance: entry 1.1037 minus stop 1.0967 is 0.0070, which is 70 pips.

- Risk per pip: $20 divided by 70 pips is about $0.29 per pip.

- Position size: $0.29 divided by the $10-per-pip standard-lot value is roughly a 0.03 lot.

For contrast, a 70-pip stop on one full standard lot would risk $700, far too much for this account. The 0.03 lot is a small, affordable micro-lot position that fits a $500-$1,000 account cleanly.

-

Then leave it alone. Once the order, stop, and target are set, the trade is a day trade. Let it hit the target or the stop, and be flat by the London close. Do not babysit it, do not move the stop to avoid a loss.

A quick reconciliation, because the numbers have to agree. Risking 2% ($20) on a 70-pip stop genuinely produces that 0.03 lot on a small account.

On most brokers 0.01 lots are the minimum, so you have room. Say you ever find a stop so tight that 2% sizes below a 0.01 lot.

That is the market telling you to skip the trade or trade a cheaper instrument, not to oversize.

Common mistakes

- Treating every hour the same. A strategy tested across all 24 hours will look worse than one run only in the London and New York windows. The strategy is not broken. It is trading in the wrong hours.

- Forcing EUR/USD into Asian hours. The pair drifts through Tokyo without conviction. If you can only trade then, switch to the yen crosses or the Aussie, where the liquidity is.

- Taking the quiet breakouts on EUR/USD. Without the volume filter you are back at a 1.08 profit factor, the noise zone. On EUR/USD, the volume spike is the edge.

- Bolting the wrong filter onto gold. Volume helps EUR/USD and hurts gold. Copying one market’s filter onto another is how a working setup turns into a loser.

- Widening the stop to dodge a loss. The stop lives on the box edge. Moving it “to give the trade room” turns a capped 1-unit loss into a disaster. The small, capped losers are the only reason a sub-50% win rate stays profitable.

- Holding past the session close. This is a day trade. Carry it overnight and you swap a known, capped risk for an unknown gap.

Honest scope: read this before you trade it

Every number here comes from one backtest on a single recent window. It is worth spelling out exactly what it covers and what it does not.

- Instruments: tested on EUR/USD, spot gold, and GBP/USD. The session-timing finding held on all three. The mechanical breakout paid on EUR/USD (long) and gold (short); it did not pay reliably on the pound.

- Timeframe and window: 1-hour bars over a recent 1.5-year stretch. A single window can flatter or punish any setup, and we flagged where the two halves disagreed on both EUR/USD and gold.

- Direction: EUR/USD longs and gold shorts, because that is what each market’s recent regime rewarded. The other side lost on each. Those are regime calls, not permanent laws.

- Volume is a proxy on forex. Currencies have no central tape, so the volume filter leans on tick volume. That is a count of price updates standing in for turnover. It worked here; it is still a proxy.

- This is education, not advice. Past results are not future ones.

Where to go from here

The whole article in three lines, if you remember nothing else:

- When: trade the London-New York overlap, 12:00-16:00 UTC, and skip the quiet pre-London hours.

- What: the London opening-range breakout, EUR/USD long with a volume spike, or gold short with the intraday trend gate. The pound does not pay.

- How: risk 2% per trade, stop on the far edge of the box, target twice the risk, and be flat by the London close.

If you want to use this, start by matching the sessions to your own day. Open a free charting account, set the clock to UTC, and add a session overlay.

Then just watch which hours your pairs actually move for a week.

Then take the London box on one instrument, EUR/USD long or gold short. Paper-trade twenty of them, tracking each as a reward-to-risk figure rather than dollars.

That is how you find out whether the setup fits your schedule and your temperament before a cent is at stake.

For the broader groundwork, our forex trading for beginners guide walks through opening an account and placing your first orders.

Once you are ready to fund one for real, our best forex brokers guide covers the options with low minimums and micro-lots for a small account.

FAQ

What are forex market hours, in plain terms?

When does the forex market actually move the most?

What are the best forex hours for a beginner?

What time does the forex market open in EST?

Is it possible to trade forex 24 hours a day?

Can you trade the London open itself as a strategy?

Why does the same setup buy EUR/USD but sell gold?

What is the win rate, and why is it under 50%?

Do forex spreads really change with the hours?

How much money do I need to start?

Should I hold a forex position over the weekend?

What do the key terms mean?

🌍 Our recommended brokers

Reader Reviews

The section on the London and New York overlap confirmed what I had suspected but never verified: my best months all had one thing in common, which was that I was trading primarily between 12:00 and 17:00 UTC without realizing it. Running back three months of trade logs showed my EUR/USD win rate during the overlap at 67% versus 51% during London-only hours, a gap large enough to determine whether a month ends positive. The spread data made it concrete: on my broker, EUR/USD sits at 0.9 pips during peak overlap and climbs to 2.5 to 3.2 pips after New York closes, so 35 trades per month at the wrong window adds roughly $27 in pure spread cost before price moves at all. Restricting all EUR/USD entries to 12:00 to 16:00 UTC helped me close last month up 7.6%.

The dead zone warning from 21:00 to 23:00 UTC stopped me from placing a trade I had been about to open on EUR/USD at 22:30 - I had been treating low-volatility hours as lower-risk rather than as periods with widened spreads and no directional conviction. Moving entries to London and overlap hours cut my average holding time from 3.5 hours to 1.8 hours with noticeably cleaner exits.

The advice to wait until 09:00 to 10:00 UTC rather than trading the 07:00 London open was something I tested over six weeks before trusting. GBP/USD breakout entries at 07:00 produced a 50% win rate - barely coin-flip territory once spread is factored in - while the same setup shifted to 09:30 to 11:00 UTC came in at 62% over the next six weeks. The explanation of why the open produces false moves gave me a reason to follow the rule rather than just adjusting my clock and hoping.

I had been trading for seven months before I understood that my strategy was not the problem - the sessions I was trading in were. Backtesting my EUR/USD breakout setup showed a 58% win rate during London and overlap hours, but live results came in at 46%, and logging my actual entry times revealed that 34% were between 19:00 and 23:00 UTC, a window where thin order flow makes breakouts unreliable. Shifting all entries to the 09:00 to 17:00 UTC window for two months brought live results much closer to backtest at 56%, with the account finishing up 6.4% and 7.8% in those two months. Thinking in session liquidity rather than just chart setup was the variable I had been missing for half a year.

The pre-NFP section named a pattern I had been experiencing without a label for it. Three times in four months I held a GBP/USD position through the Non-Farm Payrolls release and watched spreads jump to 4 pips, pushing me past my stop before price had moved 8 pips in either direction. The recommendation to close EUR/USD and GBP/USD by 12:15 UTC on the first Friday of each month and re-enter after 13:00 UTC eliminated a specific loss category from my P&L that I had been writing off as bad luck.

The session pairs table gave me a concrete answer to a question I had been researching for weeks: why GBP/USD felt unpredictable during my usual trading time of 02:00 to 06:00 UTC. Moving to USD/JPY and AUD/USD for those hours, as the table suggested, produced cleaner directional moves with tighter spreads from the first week.

Most forex session guides I had read listed the open and close times for each session and stopped there. This article went further by explaining what the session structure means for spread cost and position sizing: that a 2-pip spread versus a 0.9-pip spread on EUR/USD is not just a number but a structural cost that changes whether your strategy is viable at that hour. The worked example connecting lot size, stop size, and session timing was the kind of practical translation I had been looking for instead of another table of GMT hours.

The weekend gap risk section resolved something I had been told about but never taken seriously enough to act on. I held four EUR/USD positions over weekends in my first three months of trading, and two of them opened Monday with gaps of 22 and 38 pips against my position - both times in situations where my Friday closing stop would have protected me if I had actually used it. The article's explanation that the market closes around 21:00 UTC on Friday and reopens Sunday around 21:00 UTC, with no exit opportunity in between, shifted it from abstract advice to a concrete operating rule. I now close all intraday positions by 20:30 UTC on Fridays, and the two months since I started doing that have both finished positive: up 8.1% and 6.9% respectively, without a single weekend-gap loss.

Leave a Review

Forex Analyst & Senior Trader

Former FX desk trader with 8 years in institutional forex. Works in multi-timeframe analysis and order flow, turning desk experience into systematic, testable rules across forex and metals.